The bucks on the advancing years accounts is supposed having, better, old age. But that doesn’t indicate you simply can’t access for individuals who need to. The way you take your money from the old-age account past to help you retiring depends on this new terms of pension package, what you would like the bucks getting, and this membership you are taking they from, and many other variables. The main point is you will probably have choices-why don’t we undergo them.

Exactly what are the choices for withdrawing funds from pension profile?

The options is actually subject to brand new conditions set forth on your later years plan, therefore based on how your bundle is initiated-along with your employment reputation-talking about the you can options for being able to access retirement currency:

- Consult a withdrawal (look for less than getting exceptions to the 10% very early withdrawal punishment)

- Demand financing from the certified retirement package-401(k), 403(b), otherwise 457(b) (not available for IRAs)

- Make an application for a hardship, or unforeseen crisis, withdrawal of the appointment the requirements (not available to possess IRAs)

Look at the old-age plan’s conclusion package dysfunction (SPD) or https://availableloan.net/personal-loans-sc/central plan shows document to understand the guidelines particular to you. Your own plan’s criteria getting withdrawing currency and you will/or requesting finance can differ to what brand new Irs allows.

Withdrawals prior to attaining decades 59?-do you know the exclusions to avoid punishment charges?

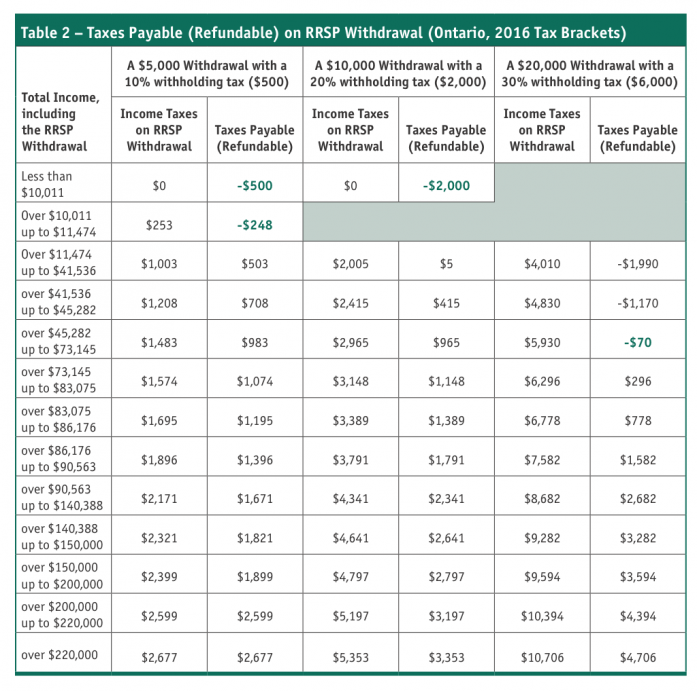

You will be usually going to spend income taxes when you withdraw pretax later years offers, whether you’re twenty five otherwise 80 years old. But when you make a withdrawal out of your later years account before many years 59?, you will be also subject to good 10% early detachment punishment, if you don’t see among the exceptions available with new Internal revenue service.

- Demise

- Overall and long lasting handicap

- Unreimbursed medical costs you to meet or exceed a specific part of their modified revenues

- Several substantially equal payments-your invest in providing costs for five many years otherwise if you do not started to age 59?, almost any comes next (repayments need certainly to start after break up from services in the licensed preparations)

- Accredited degree expenditures

- Accredited very first-day homebuyers, up to $ten,100000

۴۰۱(k) or any other package funds-that produce the borrower in addition to lender

When taking that loan from your own 401(k) package (or 403(b) or 457(b) plan), you are both borrower in addition to financial of your own money. Regardless of if that may create easier than obtaining a financial loan, it may not fundamentally create monetary feel to you. You will find trade-offs to adopt when you take financing from the later years package.

Remember-look at the SPD otherwise plan features to be certain retirement plan even offers funds and know about any particular standards when deciding to take onepare they in order to choice types of currency-a personal loan, family guarantee personal line of credit, or something relevant-to determine what helps make the really monetary experience for you.

Adversity withdrawals-what is actually believed a hardship?

An adversity withdrawal was kepted to possess activities for those who have an immediate and you may heavier monetary you would like while can not relatively find the funds from choice supply. In these instances, you could potentially withdraw extent you want and no more.

That you don’t pay back the hardship detachment-in place of a loan, it’s taxable earnings for you. Whenever that you do not qualify for an exclusion, adversity withdrawals can also be subject to new ten% very early withdrawal penalty.

Adversity distributions are not relevant so you can 457(b) plans; rather, 457(b) plans can enable unexpected emergency distributions. The two is actually similar within the heart-withdrawals for people facing monetaray hardship. In which it disagree would be the fact a trouble withdrawal are going to be a keen questioned pricing, in which an unforeseen emergency withdrawal has to be unforeseen.

Remember-look at your SPD otherwise plan highlights to make certain your retirement bundle also provides hardship or unexpected disaster distributions and you can realize about any certain conditions to take one to.

Withdrawals, funds, and you can adversity-you really have solutions

Retirement discounts shouldn’t be the first selection for bringing bucks but may be available instead of envision. What you need the bucks getting and you may if or not we should spend your self back will assist know if a withdrawal alternative or loan is acceptable. Just remember that , withdrawals expected ahead of many years 59? is actually subject to a ten% early detachment penalty, unless of course a different applies.

When you are needing money, make sure to understand the pros and cons before you can turn into the retirement makes up about financial recovery. It’s also possible to wish to get in touch with a taxation mentor or economic elite group to discuss the taxation consequences and you may economic feeling off providing an excellent withdrawal or financing from the advancing years bundle.

The content of the file is actually for general suggestions just and is thought become particular and you can reputable since this new posting big date, but may getting susceptible to alter. This is not meant to render capital, taxation, bundle construction, or legal services (except if otherwise indicated). Delight consult with your own independent advisor as to people resource, taxation, or court comments made herein.